During the last few years several reform measures have been taken with regard to the working of secondary market.

Let’s look at some of these important changes…

Rajiv Gandhi Equity Savings Scheme:

On 23rd November 2012, the government notified a new tax saving scheme called the Rajiv Gandhi Equity Savings Scheme (RGESS), exclusively for the first-time retail investors in the securities market.

This scheme provides 50 % deduction (from taxable income) of the amount invested for that year to new investors who invest up to INR 50,000 and whose annual income is below INR 10 lakh. The operational guidelines were issued by SEBI on 6 December 2012.

http://www.bseindia.com/rgess/downloads/SEBI_Notification_December_6_2012.pdf

Electronic Voting Facility made mandatory for top listed companies:

As mandated in the Union Budget 2012-13 for top listed companies to offer electronic voting facility to their shareholders, SEBI has come out with the necessary amendments in this regard on 13 July 2012, to be incorporated in the equity listing agreement by stock exchanges.

To make a beginning, based on market capitalization, electronic voting is now mandatory for the top 500 listed companies at the BSE and NSE, in respect of those businesses to be transacted through postal ballot.

SME Exchange/Platform:

Separate trading platforms for SMEs were launched and became functional at the BSE and NSE in March 2012 and September 2012 respectively. As on 14 January 2013, the number of equities listed on the BSE and NSE SME platforms is 12 and 2 respectively.

Reduced Securities Transaction Tax for cash delivery transactions:

Following the announcement in Union Budget 2012-13, the rate of the securities transaction tax (STT) has been revised downwards by 20% to 0.1% from 0.125% for delivery-based transactions in the cash market, effective 1 July 2012.

Regulatory framework for governance and ownership of stock exchanges, clearing corporations, and depositories:

Based on the recommendations of the Dr. BimalJalan Committee, new Securities Contracts (Regulation) (Stock Exchanges and Clearing Corporations) Regulations 2012 were notified on 20 June 2012 to regulate recognition, ownership, and governance in stock exchanges and clearing corporations.

Further, the Securities and Exchange Board of India (Depositories and Participants) (Amendment) Regulations 2012 have been brought into effect from 11 September 2012 to regulate ownership and governance norms of depositories.

Expansion of Qualified Foreign Investors (QFIs) Scheme:

In Budget 2011-12, the government, for the first time, permitted qualified foreign investors (QFIs), who meet the know-your-customer (KYC) norms, to invest directly in Indian MFs. In January 2012, the government expanded this scheme to allow QFIs to directly invest in Indian equity markets.

Taking the scheme forward, as announced in Budget 2012-13, QFIs have also been permitted to invest in corporate debt securities and MF debt schemes subject to a total overall ceiling of US $ 1 billion. In May 2012, QFIs were allowed to open individual non-interest-bearing rupee bank accounts with authorized dealer banks in India for receiving funds and making payment for transactions in securities they are eligible to invest in. In June 2012, the definition of QFI was expanded to include residents of the member countries of the Gulf Cooperation Council (GCC) and European Commission (EC) as the GCC and EC are the members of the Financial Action Task Force (FATF).

Initiatives to attract FII Investment:

As regards FII investment in debt securities, there has been progressive enhancement in the quantitative limits for investments in various debt categories. In June 2012, the FII limit for investment in G-Secs (government securities) was enhanced by US $ 5 billion, raising the cap to US $ 20 billion. The scheme for FII investment in long-term infra bonds has been made attractive by gradual reduction in lock-in and residual maturity periods criteria.

In November 2012, the limits for FII investment in G- Sees and corporate bonds (non-infira category) have been further enhanced by $ 5 billion each, taking the total limit prescribed for FII investment to US $ 25 billion in G-Secs and US $ 51 billion for corporate bonds (infra + non-infra). FII debt allocation process has also been reviewed for bringing greater certainty among foreign investors and helping them periodically re-balance their portfolios in sync with international portfolio management practices.

Establishment of National Stock Exchange:

An important step to provide efficient and transparent stock market culminated into the establishment of National Stock Exchange of India (NSEI) in July 1994. The NSEI opened membership to 13 cities, including Bombay, the commercial capital of India. The NSEI operates in its two segments: (i) Wholesale Debt Market (WDM) and (ii) Capital Market (CM): In the Wholesale Debt Market. Government Securities, Treasury Bills, Public Sector Undertaking (PSU) bonds, Certificates of Deposits, Commercial Papers and Corporate Debentures are traded in.

The main participants in this market are banks, financial institutions and large corporate firms. The RBI has directed banks to use only the NSEI for all transactions in debt securities instead of using the services of brokers so as to ensure transparent and regulated deals.

In the capital market, segment of NSEI, equities are traded in. In the capital market segment of NSEI, the number of securities admitted to trading has expanded from 200 to start with to 525 by December 1994. Thus, the National Stock Exchange of India (NSEI), with its scrip-less trading system, can be regarded as a milestone in the development of stock market in India.

In short, stock exchanges, as secondary market in industrial securities, furnish an important mechanism of imparting liquidity in Indian capital market. Of late, SEBI has evolved certain guidelines of rules and regulations to make stock exchanges to function in accordance with the principle of safety of the market, transparency and investor protection. The liberalisation, privatization and globalisation (LPG) of Indian economy has led to the increase in volume of business in industrial securities in both the New Issue Market and Secondary Market (stock exchange) of Indian capital market.

Mutual Fund Industry:

Of late, mutual funds have become a hot favorite of millions of people all over. The driving force of mutual funds is the ‘safety of the principal’ guaranteed, plus the added advantage of capital appreciation together with income earned from dividends.

Mutual funds scores over bank Fixed Deposits or other insurance products as mutual fund allows an investor to get into the investment game (equities, etc) with very little investment.

An investor can own blue chip stocks or high value stocks like Reliance, ITC, TISCO, HDFC Bank, etc through investment in mutual funds. Thus, mutual fund acts as a gateway to enter into high-ticket stocks even with very less investment.

In simple words, a mutual fund collects the savings from millions of individuals (small, medium and large investors) and invests the money so collected into Securities, Bonds, etc of either private, public companies or government instruments. Some mutual funds also invests in Derivative instruments, depending on what type of fund is it. Once needs to invest in the type of fund that suits my risk taking ability.

The logic of the mutual fund is simple: if one person has INR 1000 to invest, he has very little option available with him and accordingly it will fetch him limited returns. But if INR 1000 are collected from lakhs of individuals, we have with us a huge corpus of funds. This large corpus of funds when invested, many investment opportunities are available and returns are handsome, even risk can be mitigated as investment in mutual fund will ensure that investments are made in diversified manner – taking into account different instruments or different sectors.

Thus, every investor, whether big or small, will have a stake in the fund and can enjoy the wide portfolio of the investment held by the fund.

Mutual fund has emerged as a popular vehicle for creation of wealth due to lower costs, higher returns and diversified risks.

Definition:

The Securities and Exchange Board of India (Mutual Funds) Regulations, 1993 defines a mutual fund as a “fund established in the form of a trust by a sponsor, to raise monies by the trustees through the sale of units to the public, under one or more schemes, for investing in securities in accordance with these regulations. “

Origin:

The origin of the concept of mutual fund dates back to ages in human history. But the real credit of introducing the modern concept of mutual fund goes to the Foreign and Colonial Government Trust of London established in 1868. Thereafter, a large number of close-ended mutual funds were formed in the USA in 1930s followed by many countries in Europe, the Far East and Latin America. In most of the countries, both open-ended and close-ended types were popular. In India, it gained momentum only in 1980, though it began in the year 1964 with the Unit Trust of India launching its first fund, the Unit Scheme 1964.

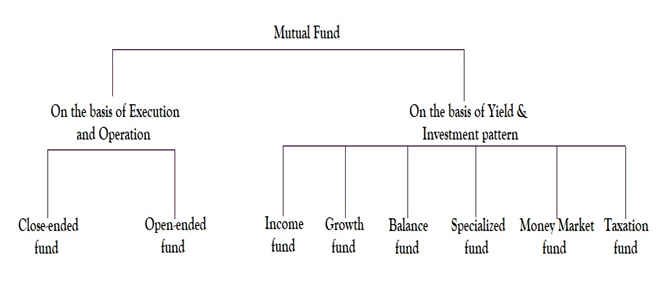

Diagram: Mutual Fund classification