Financial Market consists of

- Different types of markets (debt market, equity market, money market, etc..)

- Intermediaries

- Investors (Those who buy or sell)

- Regulatory Markets (SEBI, RBI, etc.)

- Issuers of securities

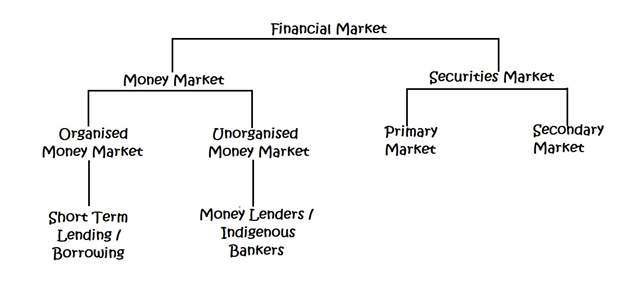

The various components of Indian Financial Markets can be illustrated through the following simple diagram:

The economic development of any country depends on the existence and growth of its well organized financial system. The major assets traded in the financial system are money and monetary assets. An efficient functioning of the financial system facilitates the free flow of funds to more productive activities and thus promotes investment. Thus, the financial system provides the intermediation between savers and investors to promote faster economic development.

The Securities markets provide a regulated framework for an efficient flow of capital (Debt and equity) from investors to various business houses. It is a systematic channel for allocation of savings to investments – not to forget the ‘risk’ element. The savings are channelized through the medium of Securities market to fund the capital requirements of business houses – it may be for expansion, normal day to day operations, acquisition of new businesses, new product launches, new markets, etc.

The term “Securities” has been defined in Section 2 (h) of the Securities Contract (Regulation) Act 1956. The Act defines securities to include:

- Shares, scripts, stocks, bonds, debentures, debenture stock, or other marketable securities of a like nature in or of any incorporated company or other body corporate;

- Derivative;

- units or any other instrument issued by any collective investment scheme to the investors in such schemes;

- security receipt as defined in clause (zg) of section 2 of the Securitisation andReconstruction of Financial Assets and Enforcement of Security Interest Act, 2002;

- units or any other such instrument issued to the investors under any mutual fund scheme (securities do not include any unit linked insurance policy or scripts or any such instrument or unit, by whatever name called which provides a combined benefit risk on the life of the persons and investment by such persons and issued by an insurer refer to in clause (9) of section 2 of the Insurance Act, 1938(4 of 1938)

- any certificate or instrument (by whatever name called), issued to an investor by any issuer being a special purpose distinct entity which possesses any debt or receivable, including mortgage debt, assigned to such entity, and acknowledging beneficial interest of such investor in such debt or receivable, including mortgage debt, as the case maybe;

- government securities;

- such other instruments as may be declared by the Central Government to be securities (including onshore rupee bonds issued by multilateral institutions like the Asian Development Bank and the International Finance Corporation);

- rights or interest in securities.

Features of Securities:

- A security represents the terms of exchange of money between two parties.

- Securities are issued by companies, financial institutions or the government and are purchased by investors who have the money to invest.

- A marketplace of all buyers and all sellers – people with surplus money to invest and issuers of securities (the ones who want to borrow funds)

- Security issuance allows borrowers to raise money at a reasonable cost

- The objectives of the issuer and the investor are complementary, and thesecurities market provides a platform to mutually satisfy their goals.

- Securities can be broadly classified into equity and debt

- An investor has the right to seek information about the securities in which he invests

Money Markets:

Money market is a market for dealing with financial assets and securities which have a maturity period of upto one year. In other words, it is a market for purely short-term funds. The money market may be subdivided into four.

They are:

- Call money market

- Commercial bills market

- Treasury bills market

- Short-term loan market

Call money market

The call money market is a market for extremely short period loans; say one day to fourteen days. So, it is highly liquid.

In India, call money markets are associated with Stock Exchanges and hence, they are located in major places like; Mumbai, Chennai, Kolkata, Delhi, and the likes.

The special feature of this market is that the interest rate varies from day-to-day and even hour-to-hour and also from center to center. The rates are highly sensitive to changes in demand and supply positions.

Commercial bills market

It is a market for bills of exchange arising out of genuine trade transactions. In case of a credit sale, the seller may draw a bill of exchange on the buyer. The buyer accepts such a bill, promising to pay at a later date the amount specified in the bill. The seller need not wait until the due date of the bill – instead, he can get immediate payment by discounting the bill.

In India, the bill market is underdeveloped. The RBI (Reserve Bank of India) has undertaken many steps to enhance this market. The Discount and Finance House of India was established in 1988 to promote secondary market in bills.

The commercial banks play a major role in this market.

Treasury bills Market

Treasury bills (better known as T-bill) has short-term maturity. A T-bill is a promissory note issued by the Government. It has a high liquidity – because its repayment is guaranteed by the Government. It is an important instrument for short-term borrowing.

There are two types of T-bills:

- Ordinary or Regular: ordinary T-bills are issued to the public, banks and to the financial institutions with a view to raising resources for the Central Government to meet its short-term financial needs.

- Ad hoc treasury bills known as ‘ad hocs’: ad hoc T-bills are issued in favor of the RBI only. They are not sold through tender or auction. They can be purchased by the RBI only. Ad hoc T-bills do not have a market of their own, but they can be sold back to the RBI.T-bills have a maturity period of 91 days or 182 days or 364 days only. Financial intermediaries can park their surplus funds in these instruments and earn income on the same.

Short-term loan market

It is a market where short-term loans are given t corporate customers for meeting their working capital requirements. Commercial banks play a significant role in this market. Commercial banks provide short-term loans in the form of cash credit and overdraft. Overdraft facility is mainly given to business houses, whereas cash credit is usually given to industrialists.

Overdraft is purely a temporary facility provided in the current account itself.

Cash credit is a separately sanctioned facility typically for a period of one year.